Rocket Fuel Newsletter – 06/11/22

This week’s edition explores the merits of FHA mortgages and how you as a Loan Officer can sell these advantages to your clients.

Fuel Up! 🚀

Biz Buzz

What goes up must come down.

So, as rates have risen quickly lately, don’t expect them to rise forever.

As China has struggled with additional COVID-19 lockdowns, their central bank has been quietly cutting rates this year.

Meanwhile, Europe is taking a slower approach – as they have struggled to generate any inflation at all over the last couple of decades.

Here at home, the Fed has stepped up with aggressive rate hikes to calm the inflation hype in the U.S. Controlling inflation would help ease the recession risk everyone keeps talking about, which stems from higher rates/inflation, but lower global growth.

Right On Target

Supply and demand are the fundamental forces at play across the globe, and we all know that COVID-19 threw a big shock into the supply of, and demand for, many goods, creating an imbalance.

This is what caused inflation – too many dollars chasing too few goods/services.

As supply adjusts to meet demand, it often overshoots.

Retailer Target warned Tuesday that it would drop its margins to clear inventory and cancel orders – the company’s inventory is up 43% year over year.

Everything must go!

Caffeinated Trends

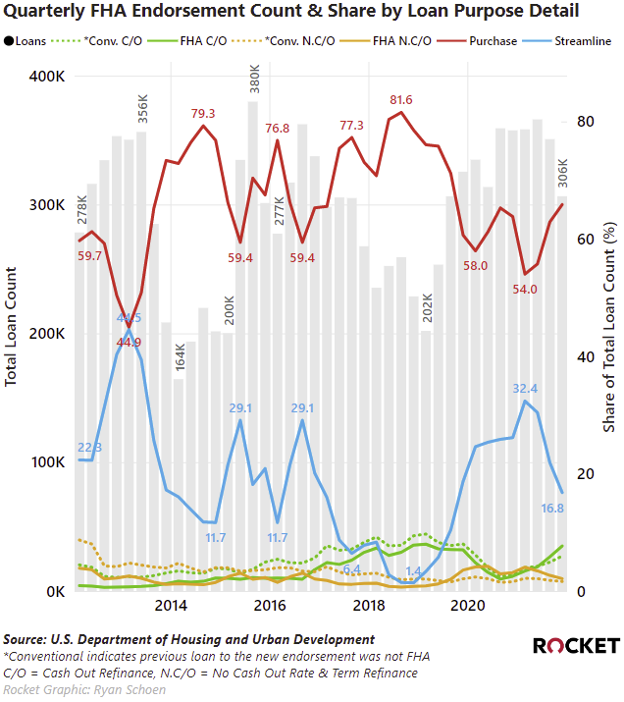

With mortgage rates and home prices on the rise, low down payment purchase loan options are back in vogue once again for borrowers and lenders alike, making FHA loans a primary beneficiary of the current environment.

Regardless of the interest rate environment, FHA is positioned as a purchase-first product, as purchase failed to account for more than half of all FHA volume for only one quarter in the last decade.

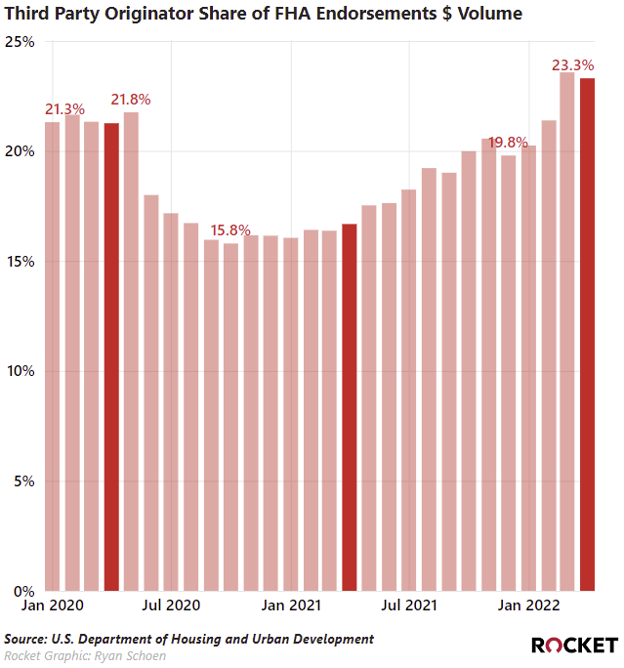

Now that the refinance boom has ended, mortgage brokers have been quick to pivot and regain their representation of more than one in five FHA dollars originated in the market.

Not only does pivoting to FHA bring in the bacon today, it also provides ample refinancing opportunities into FHA streamlines when rates fall once again or into conventional products to eliminate the lifetime mortgage insurance premiums (MIP) that exist on most FHA purchase loans.

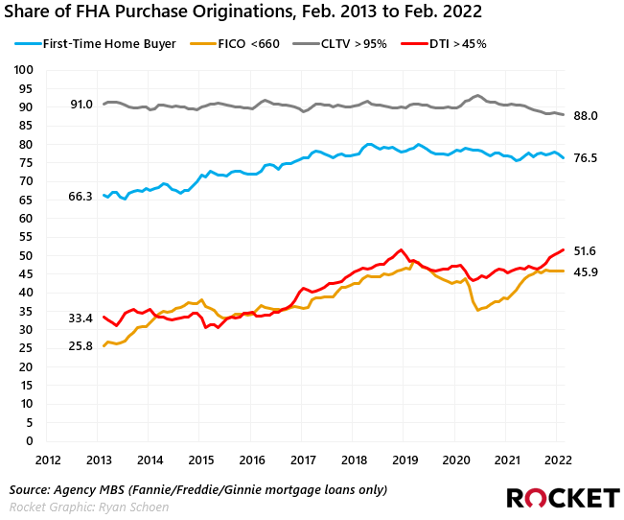

Today’s FHA purchase borrower continues to be more than likely a first-time home buyer that operates in the same low down payment range, but with increasingly lower credit scores and higher debt-to-income ratios.

With an FHA loan, the mortgage rate and MIP cost the same no matter the combination of CLTV, FICO or DTI. In fact, FHA continues to attract borrowers with riskier (higher risk of default) credit profiles. This is due to Fannie/Freddie improving their loan ladder price adjustments to promote more activity in the low down payment product space, coupled with mortgage insurance providers offering more competitive pricing across their rate cards.

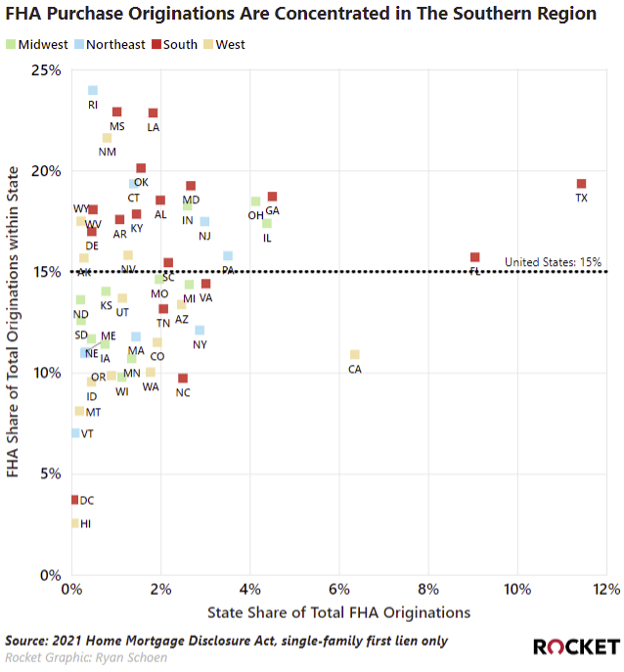

Brokers looking to pivot and focus on FHA should look no further than the Southern region of the United States. Texas, Florida and Georgia accounted for one in four FHA purchase loans originated in 2021.

Additionally, nearly all Southern states had an FHA concentration north of 15%.

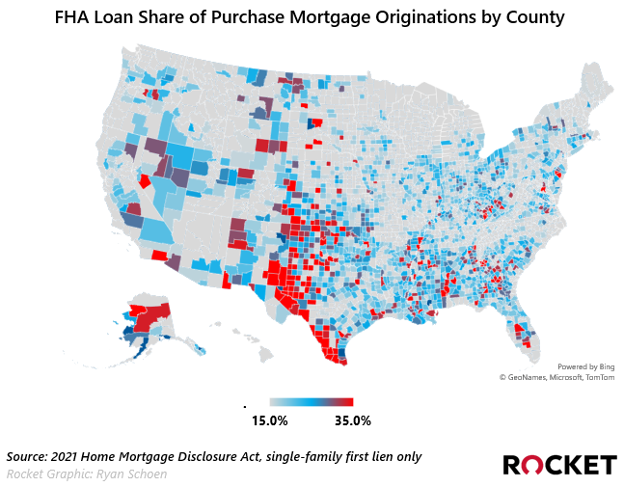

At the county level, some markets easily reach FHA concentration levels that are more than double the national 15% mark.

Bonus selling tip: If you are working with a homeowner who is currently an FHA borrower and they are having trouble selling their existing home, do not forget that FHA loans offer a hidden benefit not available on conventional loans: the ability for the next buyer to assume the existing FHA mortgage. If a home buyer qualifies for the existing terms of an FHA mortgage, they can assume the existing loan and its original interest rate. That means that as interest rates increase, your FHA loan makes your home a much more attractive option.

Partner Spotlight – Ty & Wendy Cline, Stratify Lending

Favorite things about Rocket:

- Pricing Calculator: “In the old days you’d have to take the base rate and add in the LLPA’s to get the final rate. Now our LO’s can price out a loan in literally 30 seconds.”

- Pathfinder: “Regulations are constantly changing and it’s good to have a place to go to keep current.”

- Team Members: “Don’t be afraid to voice an issue because you guys are really good at listening.”

First job: Restaurant cashier/server (Wendy), Grocery story bakery cleaner (Ty)

First mortgage industry job: Recruiter (Wendy), Loan Officer in the mid-‘90s (Ty)

Coffee/tea preference: Iced tea (Wendy), Diet Coke (Ty)

First concert: KISS (Wendy), Mötley Crüe (Ty)

Local delicacy (Salt Lake City): Funeral potatoes – au gratin potatoes with corn flakes toasted on top

There’s no questioning the value of FHA loans for home buyers – millions of Americans take advantage of the lower down payment requirement to buy their first homes, even if it means taking on mortgage insurance (MIP). When those buyers are ready to refinance and ditch the MIP, brokers like Stratify Lending in Salt Lake City, Utah, are there to help.

Husband-and-wife team Ty and Wendy Cline started Stratify Lending in 2017 with the intention of focusing their business on FHA loans, which includes FHA Streamlines, purchase loans for first-time home buyers and even refinance loans to get clients out of their MIP-laden FHA loans.

The latter loan purpose – removing MIP by refinancing an FHA loan into a conventional loan – is Stratify’s #1 priority, according to Ty and Wendy.

“If someone’s been in their house 12-18 months, they have enough equity to get out of MIP, and if they’ve been there 24+ months, you have enough equity to also save people money.”

How does the Stratify team get these clients in the door? Although Ty and Wendy ultimately chose to stay in the brokering game because of the rate of growth in mortgage technology, they credit old-school direct mail campaigns as their primary driver of business.

“If [we] direct marketed Conventional instead of FHA borrowers, the response rate [on Conventional] would never pay off. You’re beating yourself up on Conventional loans – someone will always write the loan cheaper.”

Ty and Wendy are all about strategy when it comes to their FHA-targeted direct mail – their team mails based on FICO, when the client bought their home, when they last refinanced, loan type and other factors. According to Ty and Wendy, at one point every single person that called in was in an FHA loan and looking to refinance.

This strategy has worked both in their home state of Utah and has also allowed them to scale across the country. The old-school approach of direct mail marries well with today’s technological advancements and smartphone culture – brokers just have to get the borrowers’ attention first.

“Clients don’t care where you are. [Especially after] COVID, you don’t meet anyone anymore. Everything is done online and over email/text.”

Regardless of the state or which marketing channel brought the borrower to Stratify, Ty and Wendy simply want to help their clients save more money each month.

“If your boss came in and said they’re giving you a big raise, you’d start crying. You’re basically doing the same thing – giving the client a big raise in their income. It’s life-changing for people.”

In The Weeds Reads

1. CoreLogic Forecasts Decreasing Rate Of Home Price Growth

2. Existing Mortgage Holders Gain Record $1.2T In Tappable Equity In Q1

3. Mortgage Credit Availability Decreased In May

4. Only 17% Of Consumers Reports It’s A ‘Good Time To Buy’

5. Single-Family Home Building Growth Slowing In Large Suburbs

Pro Puzzles

Pamela’s time of 1:11 led all solvers on a tough puzzle last week – just four other solvers were able to complete it in less than 2 minutes.

This week’s puzzle gets 3 Rockets out of 5.